India’s trucking sector moves approximately 4.6 billion tonnes of freight annually. As this critical industry expands, truck owners and businesses relying on trucking services must understand how Goods and Services Tax (GST) applies to their operations. This guide covers GST implications for both Goods Transport Agencies (GTA) and truck owners, exploring rates, schemes, and available exemptions.

What is GST?

GST (Goods and Services Tax) is a comprehensive indirect tax on the supply of goods and services in India. Registration requirements vary:

- Normal States: Annual turnover exceeding Rs. 40 lakh requires GST registration

- Special Category States: North-Eastern and hilly regions have lower thresholds at Rs. 10 lakh annually

I. GST for Goods Transport Agency

GTA Meaning (Goods Transport Agency)

According to Central Tax (Rate) dated 28/06/2017, a Goods Transport Agency is defined as a company that transports goods by road and issues a receipt, known as a consignment note. GTAs act as intermediaries connecting shippers with carriers while handling logistics, documentation, and insurance.

GTA Services Under GST

GTA services include:

- Issuing serially numbered consignment notes for tracking goods

- Arranging packing, loading, unloading, and storage

- Ensuring safe, timely goods delivery

- Managing shipment paperwork and documentation

Consignment Note Under GST

The GTA issues serially numbered consignment notes upon receiving goods for transport. This key document outlines:

- Consignor (sender) and consignee (receiver) details

- Goods description and quantity

- Origin and destination

- GST payment responsibility

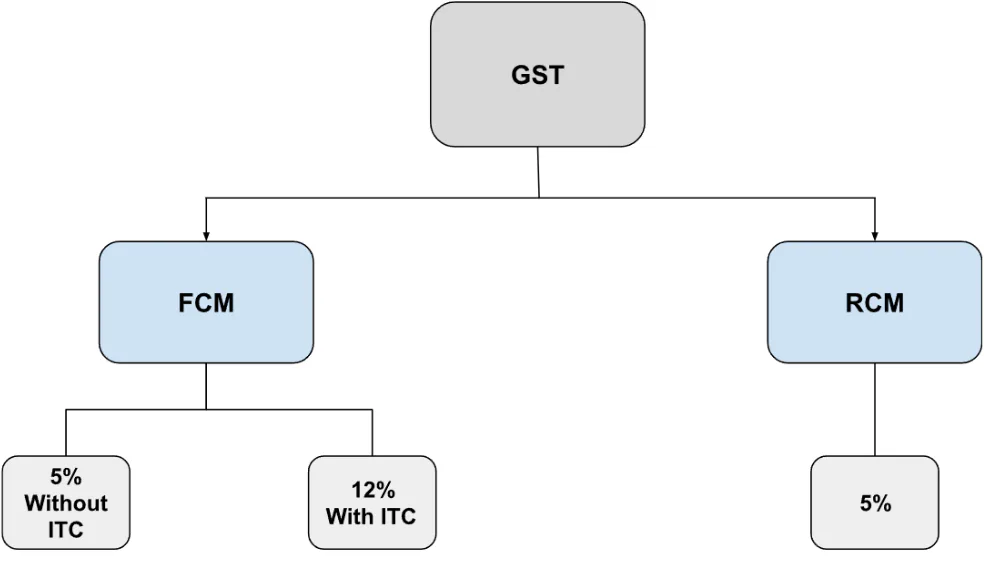

GST Rate on GTA

Registered GTAs must charge GST on transportation services. The payer varies depending on the circumstances.

Forward Charge Mechanism (FCM)

The GTA itself pays GST, with two options:

1. 5% GST Without ITC:

- Simpler structure

- GTA charges recipient 5% and pays government directly

- Cannot claim Input Tax Credit on business purchases

- May increase overall operational costs

2. 12% GST With ITC:

- Allows claiming ITC on eligible purchases (fuel, maintenance, etc.)

- GTA charges recipient higher rate (12%)

- Requires detailed record maintenance

- Potentially reduces overall tax liability

Returns Filed by GTA:

- GSTR-1: Monthly/quarterly return detailing outward supplies

- GSTR-3B: Monthly/quarterly summary of tax liability

- GSTR-9: Annual return providing comprehensive transaction overview

Reverse Charge Mechanism (RCM)

The recipient pays GST at a flat 5% rate. GTAs need not file GSTR-1 or GSTR-3B under RCM, though GSTR-9 may be required depending on overall transactions. This applies when recipients fall under specific categories:

- Factories (under Factories Act, 1948)

- Registered societies and co-operatives

- Body corporates and PSUs

- Partnership firms (registered or unregistered)

- Any GST-registered business

- Casual taxable persons

GTA Exemptions Under GST

1. Based on Specific Goods:

- Agricultural produce

- Milk, salt, and food grains

- Organic manure

- Defense/military equipment

- Newspapers and magazines

- Relief materials

2. Based on Transaction Value:

-

- Single consignment transportation charges not exceeding Rs. 1,500 are exempt

-

- Total charges for all goods to a single consignee below Rs. 750 are exempt

Based on Entity:

-

- Central and state government departments

-

- Local authorities and governmental agencies

II. GST for Truck Owners/Small Fleet Owners

When purchasing new trucks, GST applies at 28%. For example, a Rs. 40 lakh truck incurs Rs. 11.2 lakh additional GST. However, owners may claim this as Input Tax Credit.

1. Operating Truck Yourself

Registered Business (FCM): Responsible for collecting and depositing GST with the government at 12% rate with Input Tax Credit eligibility.

Unregistered Business (RCM): May fall under RCM in certain situations when receiving services from larger GST-registered companies. Shippers pay 5% for taxable goods.

2. Renting Truck to a Goods Transport Agency (GTA)

Renting trucks to GTAs is exempt from GST, regardless of the owner’s GST registration status. No GST collection or payment is required in this arrangement.

Summary Table

| Scenario | FCM (Forward Charge Mechanism) | RCM (Reverse Charge Mechanism) |

|---|---|---|

| GTA / Large fleet owners | 12% with Input Tax Credit | Shippers pay 5% for taxable goods |

| Small fleet owners renting to GTA | Not Applicable (Exempt) | Not Applicable (Exempt) |

| Small fleet owners renting to shippers directly (not through GTA) | 12% with Input Tax Credit. Most truck owners lack GST registration and don’t opt for FCM | Shippers pay 5% for taxable goods |

Conclusion

Truck owners and GTAs operate as vital components of India’s logistics network. Understanding GST enables efficient navigation of the system and ensures smooth business operations. For situation-specific guidance, consulting with a tax advisor familiar with the trucking industry is recommended.